Making History: An Overview of the First Five Parachain Slot Auctions on Kusama

This post provides important background information on the candle auctions and crowdloan mechanisms for these slots and recaps what happened during the first five auctions.

By Polkadot•August 18, 2021

By Polkadot•August 18, 2021

by Jonas Gehrlein, Web3 Foundation Research Scientist

Introduction

The launch of the first rotation of parachain slot auctions on Kusama marks a major milestone in achieving a scalable, decentralized, and interoperable future, with several professional teams ready to compete for and launch on one of the first five ever available parachain slots. This post provides important background information on the candle auctions and crowdloan mechanisms for these slots and recaps what happened during the first five auctions. It uses data available from the Kusama blockchain as well as results from an anonymous survey that was conducted with fifteen parachain teams prior to the auctions (at the end of March / early April). Furthermore, the last section incorporates information gathered from oral interviews with parachain teams about their expectations of the parachain slot auctions, especially in the future when some parachains will be aiming to extend their leases while others are simultaneously seeking their first onboarding.

The Candle Auction: A refresher

Before proceeding with the analysis of the individual auctions, it is good to summarize the underlying mechanism. The candle auction is an old auction format from around the 16th century where bidding was allowed until an actual wax candle went out. The uncertainty about the actual ending time of the auction was used to reduce auction sniping, which was an issue even back then. In auction sniping, bidders squeeze their bid in at the last possible moment, so that other participants don’t have the chance to react with a higher bid. Many of us probably had similar experiences in the past with online auction formats such as eBay.

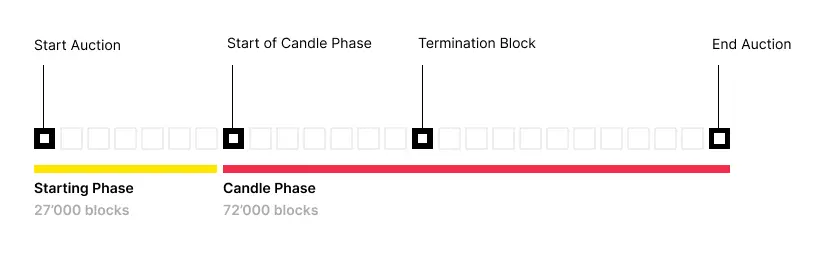

The candle auction format was long considered exotic and has not seen much application. However, it has proven beneficial properties when combined with blockchain technology, both for avoiding sniping and obtaining efficiency (see here for further details). It is therefore considered to be a suitable mechanism to allocate parachain slots on Polkadot and Kusama. In contrast to the ancient candle auction, the end is determined retrospectively. That means, the auction always has a fixed length of time for bidding, and the actual ending block (“termination block”) is randomly determined only after this. We can mark four important checkpoints to describe the temporal procedure of a candle auction, described in block heights. The following graph illustrates the structure.

The start and end blocks of the auction determine the fixed length of each auction and give participants certainty about the overall framework. The first phase of the auction, lasting exactly 27,000 blocks (around 45 hours), serves as a grace period where teams and users have time to get an overview of the situation, gather information, and set up their bidding/contributing strategies. Although bidding is enabled, the blocks in this phase are not yet considered by the mechanism, i.e., the termination block cannot fall inside that range. After that, the candle phase (or ending phase) marks the “real” beginning of the auction. Here, figuratively, the candle is lit and this phase lasts for 72,000 blocks (around 5 days). During this phase, the auction could end at any given block with equal probability (i.e., the candle phase has a uniform termination profile).[1] Bidding is allowed until the end of the auction. After the official ending, the termination block is computed by using a combination of verified random functions (VRF). Calculating the termination block retrospectively ensures that nobody can predict it before or during the auction.

The winning bids that are contained in the termination block are then used to determine the outcome of the auction, while all later bids are discarded. This uncertainty and the possibility that bids are not relevant for the final outcome incentivizes early bidding and can thereby reduce sniping. To keep potential confusion of participants at a minimum, there can only ever be one active auction at any time.

Crowdloan Mechanism

Technically, a crowdloan is a simple module that enables projects to gain support for their parachain in a decentralized way. Specifically, tokens are gathered on behalf of the teams, and remain in the custody of and are secured by the Relay Chain. This means that participation in a crowdloan campaign is trustless for users and they can be certain to receive their contributions back at one of two predefined dates. The first date corresponds to the case where a project’s crowdloan successfully secured a parachain slot. In this case, tokens can be reclaimed by the users at the end of the lease that the crowdloan obtained. In the other case, tokens can be retrieved directly after the (generally short) duration of the crowdloan expires. As tokens are reclaimable, the actual costs of users’ contributions, economically speaking, are the opportunity costs that accrue from locking those tokens (e.g., forgone rewards from staking or from using the tokens differently). To provide clarity about when users can expect their tokens back in the event that the crowdloan wins a slot, the leasing period that it bids for is fixed. Additionally, as a contribution is made the crowdloan module automatically increases the bid by exactly that amount.[2] If the crowdloan successfully wins an auction, tokens are automatically locked for the period of time and then released and can be reclaimed by the accounts that contributed. Contributions after the termination block (but before the end of the auction) are still locked, but naturally did not increase the winning bid. Any incentive structure for contributing to the crowdloans are completely organized by the respective crowdloan projects.

Auction Schedule

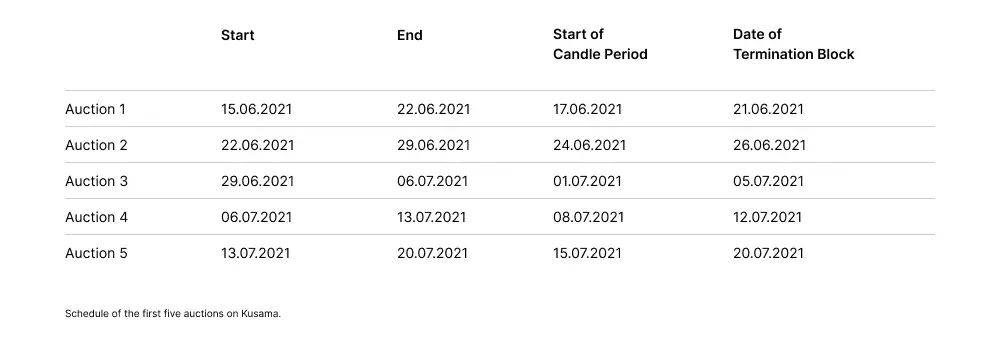

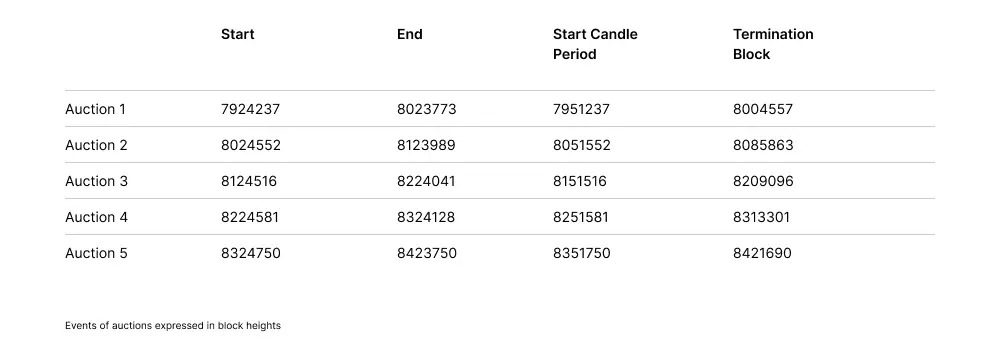

After having established the basic concepts, let us dive into the data. In total, the first rotation allocated five parachain slots during June and July 2021. The whole campaign lasted from June 15th and the last auction ended on July 20th. Each auction lasted seven days with a two-day starting and five-day candle phase. The following table provides the dates for the four important events of each auction (the same table with the events expressed in their block heights can be found in the Appendix).

Auction Data

All bids were cast by crowdloans.[3] This was to be expected as in the survey, 86.7% of projects predicted that they would use crowdloans to support their bids. The rest either changed their strategy in the meantime or aim to bid from a user-controlled account in future sequences of auctions. Most projects claimed that their project requires a lease period of at least one year to fully operate, which is why all crowdloans were programmed to bid for the entirety of 8 leasing periods (labeled 13-20), which roughly corresponds to 48 weeks.

Overview

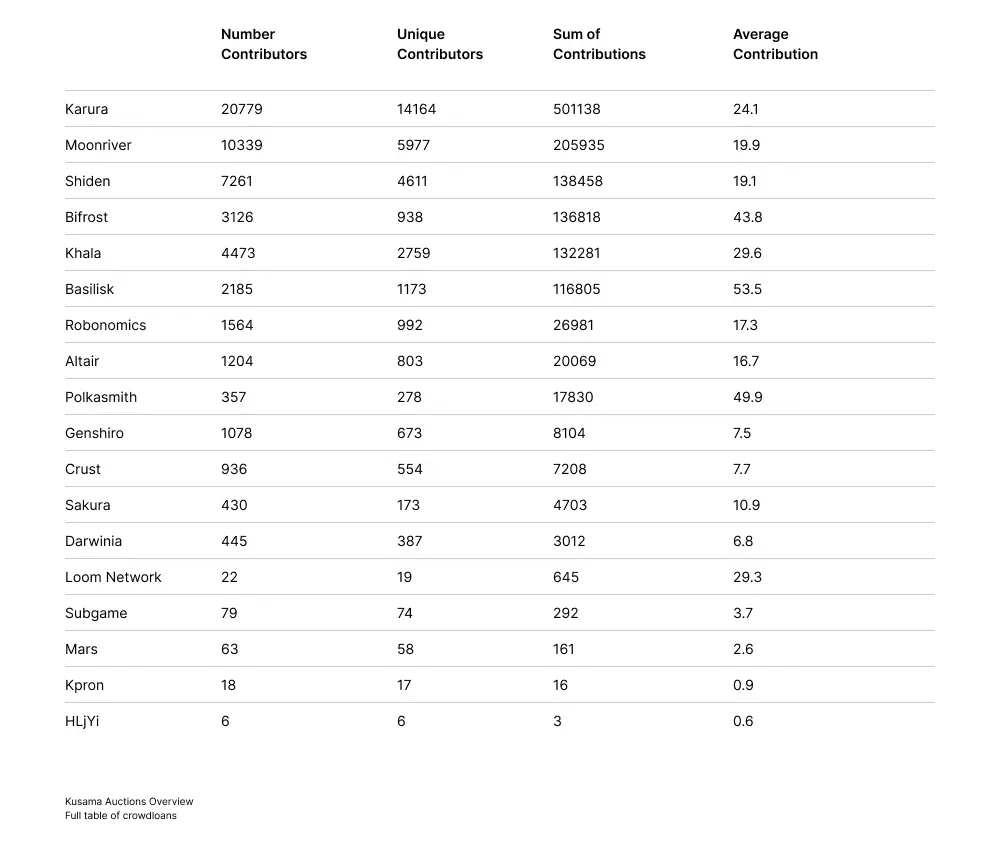

Already at the time they took the survey, the teams felt ready for the long-awaited start of the parachain slot auctions on Kusama. Ten out of 15 teams indicated that they were aiming to enter the race for the first available slots on Kusama. Most of the teams (80%) indicated that they also plan to launch on Polkadot (with 13.3% only on Kusama and 6.7% only on Polkadot). The survey shows that the strategies and preparation for the auctions were a high priority for the teams, as they gave it extensive thought (with an average score of 6.5 of 7). It is therefore not surprising that we saw fierce competition between teams in securing their spot on the Kusama Relay Chain. In total, 18 crowdloans registered to participate in the auctions and received contributions during the campaign from 19,017 unique accounts. A total number of 1,320,458 KSM was bonded for crowdloans. Of these, 1,114,629 KSM has been locked in slots until May 13th, 2022, while the rest can be reclaimed by users as their chosen crowdloans didn’t secure a parachain slot. At the time of the events, from all issued KSM tokens, 47% is locked in staking and 9.9% for crowdloans. Individual accounts contributed on average to 1.8 crowdloans (for more details, see Appendix).

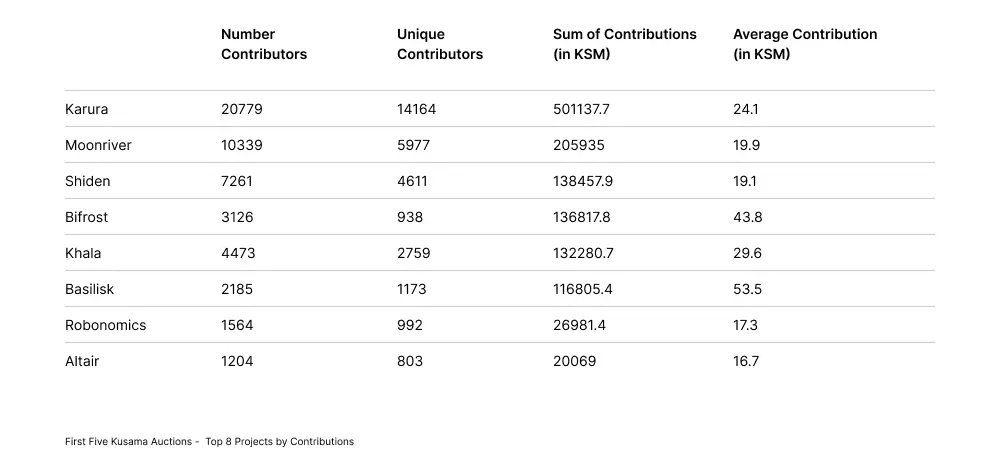

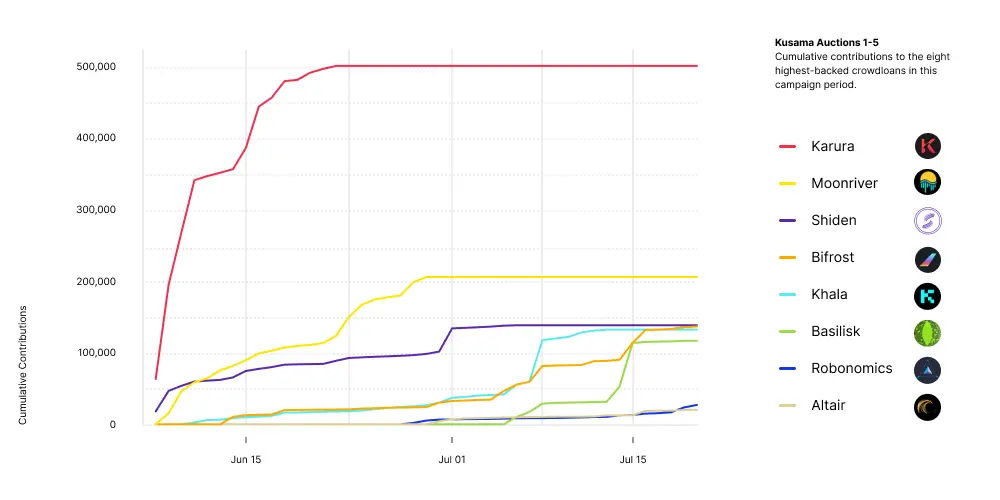

The following table summarizes relevant metrics for the eight projects with the highest locked KSM for crowdloans (the full table is available in the Appendix).

The following graph shows the cumulative contributions of the eight highest-backed crowdloans for the whole campaign. This gives some visual insights about the contribution dynamic of the different projects. We can spot a clear hierarchy between the contribution levels for the first three auctions, while things get more dynamic for the fourth and fifth auctions. As all bids were made for the same leasing periods (full duration of the slot), contributions can be compared within a single graph. After a crowdloan successfully wins an auction contributions are no longer allowed and therefore the curve flattens out for the winners.

We’ll have a closer look at each auction in the following section.

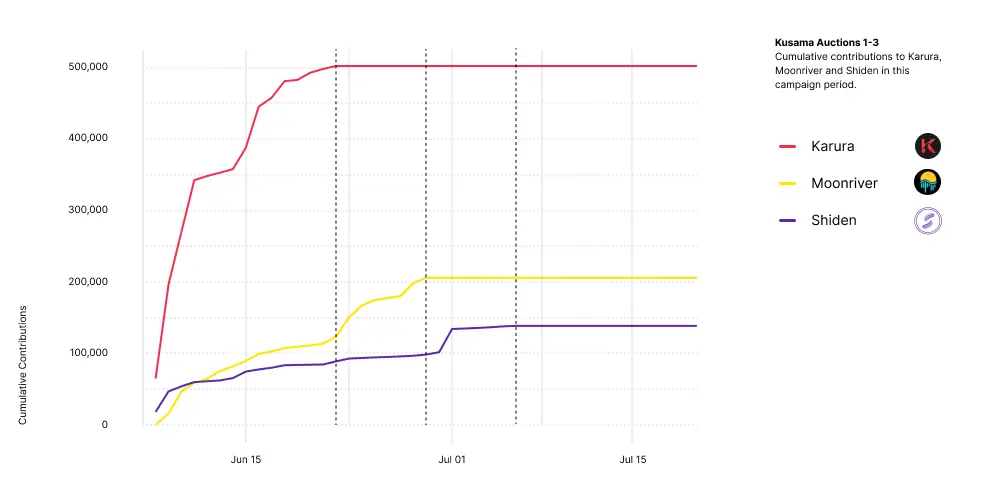

Auction 1-3

From the very beginning, three strong teams crystallized and consequently it was no surprise that they occupied the first three slots on Kusama. Karura took the lead early on and surpassed all other teams by a large margin. Moonriver started out lower than their competitors but was able to quickly surpass Shiden even before the candle phase started. Shiden secured the third spot. In total, 501,138 KSM was bonded to support the Karura slot; 205,935 KSM for Moonriver; and 138,458 KSM for Shiden.

The following graph illustrates the dynamics of the crowdloan contributions of those three projects aggregated on a daily basis. The vertical lines correspond to the ending dates of the respective auctions.

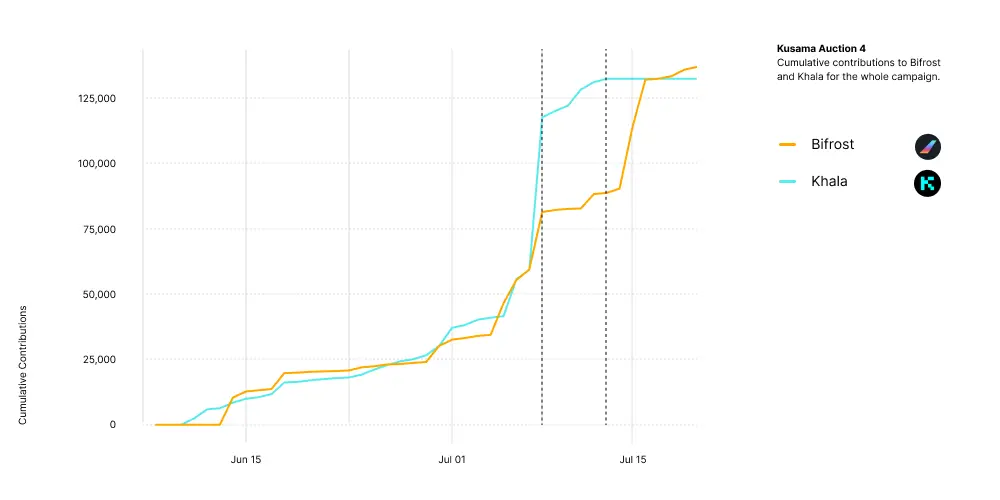

Auction 4

In contrast to auction 1-3, the fourth auction was, especially in the pre-candle phase, more dynamic. The main contestants were Bifrost and Khala. The leading position switched periodically in this head-to-head race, as the following graph illustrates. The first vertical line indicates the start of the candle phase and the second vertical line the end of auction 4.

The highest bid constantly changed before the candle phase started. However, Khala secured large contributions just as the candle phase started and held the highest bid during all blocks. This can mainly be attributed to the candle mechanism, where it is important for teams that want to maximize their winning probability to secure the lead throughout the whole candle phase. Bifrost was, indeed, not able to catch up and therefore Khala won the fourth parachain slot on Kusama. In total, 132,280.7 KSM was bonded for their crowdloan.

Naturally, Bifrost was still in the race for the fifth and last slot and contributions kept increasing after the end of the fourth auction.

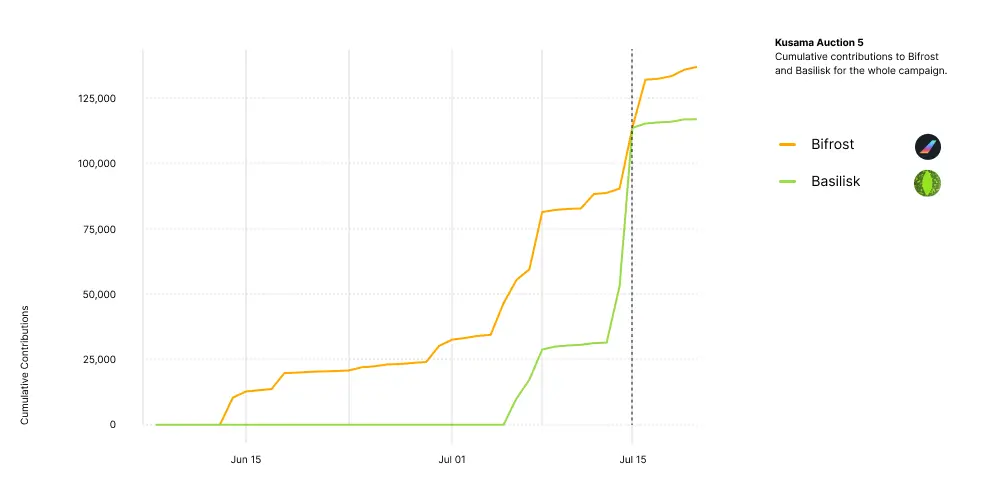

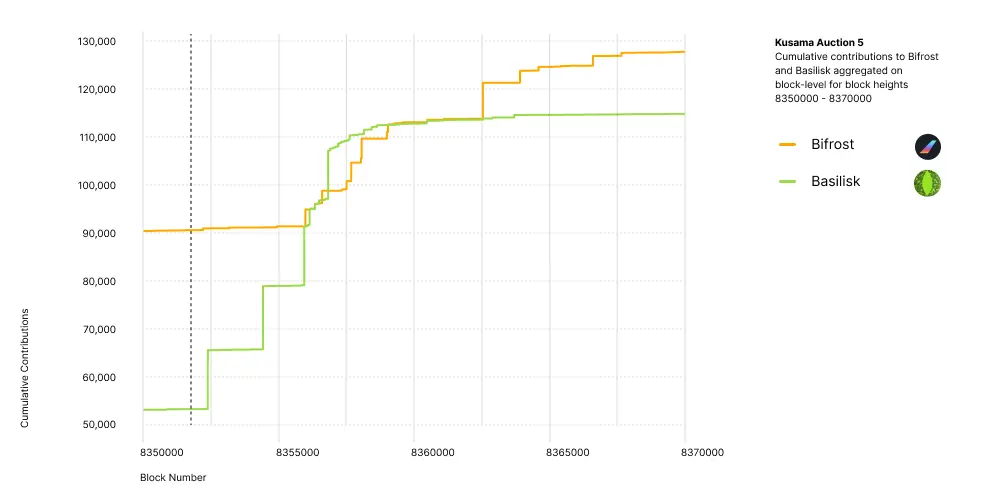

Auction 5

In a strong position from the fourth auction, Bifrost continued to compete for the last available slot. At first, it looked like it would be an easy win, as no other project came close to their contribution level. However, a strong competitor, Basilisk, started their crowdloan shortly before the start of the fourth auction and promised fierce competition for Bifrost. Basilisk’s crowdloan gained traction and caught up quickly. The vertical line indicates the beginning of the candle phase.

While the pre-candle phase was easily led by Bifrost, Basilisk managed to come very close to Bifrost at the important start of the candle phase and the winning bids even switched between the teams during that period. To get a better look at the details, the following graph increases the resolution to cumulative contributions aggregated on the block level.

We can see that Basilisk had the highest bid in a few blocks in the decisive candle phase. Therefore, theoretically, both teams could have ended up winning the auction. However, Basilisk could not sustain their pressure and Bifrost’s position was too strong. Because they led 96.6% of blocks during the candle phase, Bifrost was heavily favored by the odds to win. Given that every block has the same chance of being pivotal for the outcome of the auction, this also corresponded to a 96.6% chance that they would win.[4] In the end, we did not see a big surprise and Bifrost obtained the fifth auction, with 136,818 KSM bonded in the process. Interestingly, that number exceeds the bonded tokens for slot 4.

The Impact of the Candle Mechanism

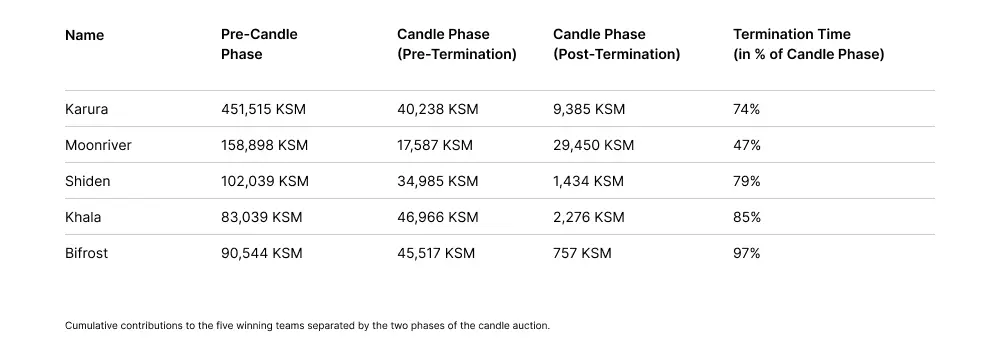

As explained in the introduction, the candle auction is composed of two different stages, namely the starting and candle phase. The latter is further divided (retrospectively), into a period that falls before and after the termination block. This mechanism could lead to the situation that the highest bidder at the end of the auction does not necessarily win the auction, because their winning bid is discarded if it falls into the range after the termination block. All tokens that are contributed to a winning crowdloan during the whole auction would still be locked for the entirety of the respective leasing period. This means that we could observe some inefficiency, both in determining the winner and in locking tokens that did not contribute to a higher winning bid. In the next table, the sum of contributions is separated by the respective phases. Additionally, the table shows when the termination block occurred as a percentage of the whole candle phase.

In general, the auction mechanism aims to incentivize individual bidders to bid early. It is difficult to assess how it influences the contribution pattern of many users that are bonding their tokens for crowdloans. Further, as early bids were retained for consecutive auctions, it is not clear whether we would have seen the same bidding dynamics in single auctions. Another confounding factor is that some teams provided stronger platform rewards for early contribution, which blend with the incentives provided by the candle mechanism.

However, taking the data of the first auction as a proxy, it seems that incentives to act early worked, as most of the contributions were made in the pre-candle phase. For the other auctions it was harder to judge because contributions could be made at any time before the auction. However, most contributions for the crowdloans that eventually won were made in the pre-candle phase of the respective auction. It therefore seems that the candle mechanism successfully incentivized early bidding. There was, however, some amount contributed after the termination block which could have led to inefficiencies.

Summary

The arrival of slot auctions to the Kusama network marks an exciting time for the entire Polkadot ecosystem and for blockchain as a whole. With the advent of parachains, we made a big step towards a scalable, decentralized, and interoperable future. The first five projects that went live are Karura, Moonriver, Shiden, Khala, and Bifrost. Those projects are about to add great functionality to the Kusama ecosystem by providing the infrastructure for DeFi, liquidity solutions, smart-contracts (both native and EVM compatible), confidential cloud computing, and more.

In evaluating the overall outcome, auction theory proposes two main properties. First, the efficiency, which dictates that the bidders with the highest valuations receive the goods. This is closely related to our perception of fairness and is therefore a desirable property. The second dimension is the revenue that is created, i.e., the prices that were paid for the goods by the bidders. Generally, those properties are hard to assess in real-world scenarios. The “value of the goods” (for example a slot) is a theoretical concept and in reality is influenced by many factors. To get a better understanding it is useful to have a more controlled environment. Experimental investigations have proven useful to obtain quantifiable benchmarks in assessing auctions and different their formats.

That being said, we can still take a closer look at the results with those concepts in mind. If we take the total backing for the crowdloans as a proxy for the valuation that would be created by the respective projects occupying those slots, we can summarize that the five teams with the highest backing received the five available slots. Specifically, the candle mechanism did not lead to the case where a slot was allocated to a project that had less backing at the end of the campaign than another project that did not obtain a slot. The second property of evaluating standard auctions, revenue, is also hard to assess in this special case. As there is no entity that could be considered an auctioneer, there is nobody directly benefiting from bids, and therefore we cannot argue that any revenue was created.

Another observation is that especially for slot 1 and 2, an excessive number of tokens was bonded (compared to the second-highest bid). From the theoretical perspective, this could be considered as not optimal, because more tokens than necessary were bonded to win the slots. However, in reality there are some influences to account for that, especially during this onboarding phase, where all teams aimed for their inception. First, the distribution characteristics of the crowdloans are more important than minimizing the winning bid in the auction. It was simply more useful to distribute the tokens to as many supporters as possible in order to benefit from future network effects and to build an involved community. Second, more backing signals a higher quality and value of the project to the ecosystem. Third, the opportunity costs of the excess of bonded tokens was shared among the contributors, who received compensating platform rewards. Those factors outweigh the importance of obtaining a slot as cheaply as possible. We will see in the next section that this might change in the future.

Another mechanism offered by the candle auction that we have not yet seen in action is the possibility that lease periods can be combined and shared between different bidders. The absence of this option to date can be attributed to both the present incentives in the onboarding phase and the resulting use of crowdloans, which were all set for the full slot duration. In particular, any bid for less than the full slot duration was destined to lose. This had already been anticipated by the teams; in the survey 80% claimed they would program their crowdloan to bid for the full slot duration.[5]

Another specialty that arises due to the fact that several slots were auctioned off consecutively, is the following economic rationale. Similar to a horse race that has already started, users were able to predict the outcomes for most of the auctions in advance. We saw that, only with the exception of auction 5, there was a strongly leading crowdloan before the start of each respective candle phase. Due to the fact that the tokens would be locked for at least the duration of the whole campaign, a vote on a crowdloan that was very likely to lose was an economically costly decision. Therefore, users not only needed to evaluate which team they would prefer to win, but also which team would be likely to win. Especially later in the campaign it became increasingly difficult for teams to catch up to leading teams, because many users might have felt discouraged contributing to lower-backed crowdloans. So, their rational choice was to either contribute to a winning crowdloan or not to participate at all. This rationale might have increased the distance between teams as time passed on.

In conclusion, the outcome of the auctions was largely shaped by the overwhelming use of crowdloans and their specific implementation. While from a purely theoretical perspective we observed some unusual factors, most of them can be accounted for by the nature of the onboarding phase. Generally, the candle mechanism seems to have incentivized earlier bidding (or contributing) and the highest-backed teams won their respective slots.

The Future

With more auctions upcoming, it is worthwhile to consider how things could develop in the future. Naturally, it will evolve from the situation with no active parachains to a situation where some parachains will need to sustain operations by extending their leases while others are aiming to be onboarded for the first time. This will lead to more dynamic events where the two main aspects affected in the campaigns are the contribution mechanisms themselves and how tokens are then used in auction bidding. Currently the spotlight is on the contribution mechanism, i.e., the crowdloans, which already comes with a pre-built bidding mechanism. However, we might see the bidding aspect become increasingly important, therefore needing to be more dynamic. That is due to the fact that the economic incentives for projects that seek to extend their leases will be different from those that need to be onboarded for the first time. Additionally, the maturing ecosystem with the previously-mentioned functionalities, enabled by interoperable chains, offers new possibilities for more dynamic bidding strategies. Let us disentangle the two mechanisms and look at them individually.

Contribution Mechanism

Most ambitious projects require external support long before the final product is even close to completion. This holds true for crypto- as well as traditional markets. In previous token generation events on other chains, generally all contributed tokens were collected at a premature state and their ownership was fully transferred to the founding teams. This often led to the case that the work almost immediately stopped, the development stalled and supporters endured large losses.

In contrast, crowdloans are a trustless and decentralized device to enable the community to vouch for their most favored projects, while the ownership of the token remains with the contributor, bonded to the trusted Relay Chain. In return, teams receive the chance to benefit from the valuable infrastructure that has been built around the Kusama and Polkadot networks and start delivering on their vision. Crowdloans, therefore, are an innovative way to tackle the underlying incentive problem that occurs in this situation. In some sense, it helps to bootstrap the projects while incentivizing ongoing effort, as teams want to prove that they have a meaningful place in the ecosystem. The scarce nature of the parachain slots ensures healthy competition in the future and helps to find and filter the most suitable projects. This novel contribution mechanism will improve the overall quality of the ecosystem, contributing to a healthy environment where users can feel comfortable supporting new projects.

Having spoken to a few leading parachain teams, it is clear that sourcing support from the community in the form of crowdloan contributions remains an important part of their economics in the future. Aside from the fact that the burden of opportunity costs can be shared, teams especially enjoy it as a mechanism to efficiently distribute their native token to a large crowd of supporters. As teams are innovative, they are already looking for suitable alternative contribution mechanisms to incorporate into their infrastructure. One reasonable direction is a parachain-native variation of the crowdloan pallet that leverages the interoperability of chains. For example, users could deposit their parachain-native token to a smart-contract that automatically exchanges them, via a decentralized exchange (DEX) parachain, to Relay Chain tokens (i.e., KSM or DOT). The smart-contract could then automatically use those tokens to bid in the auction. In addition to the parachain’s native tokens, with upcoming bridges to Ethereum and Bitcoin, it is even possible that the smart-contract could use ETH (and erc20 tokens) and BTC.

In the survey, teams claimed to aim for a ratio of own tokens to crowdsourced tokens of, on average, 21% already in the first auctions. This percentage of non-community tokens will likely need to increase in the future, as it would become increasingly difficult to offer platform rewards for contributors as the initial native supply will eventually be fully distributed. Teams further expressed a desire to extend this hybrid approach where tokens are both sourced from the community and supported by the team’s own treasury. Similar to the smart-contract solution described before, parachains might evolve into decentralized autonomous organisations (DAOs) that raise tokens during their operation and accumulate them within their on-chain treasuries. Eventually, in order to secure preservation, the chains might start to accumulate Relay Chain tokens in this way to extend their leases. That means, the chains themselves are increasingly becoming self-sufficient.

Auction Bidding

As explained before, the onboarding phase is a unique situation in the network, where minimizing the winning bid is not the most important factor. Therefore, we saw the focus on maximizing the bonded tokens rather than optimal bidding under the auction mechanism itself. However, once the network reaches the extension phase some active parachains will need to secure consecutive leases, competing with new projects that aim for their first onboarding. By then, the ending period of one slot will likely overlap with lease periods of several other slots. Then, it becomes increasingly useful to strategically evaluate which auctions to participate in. It would even make sense to withdraw from one auction when bids are getting too high, just to join bidding in another.

In such a situation, flexible bidding, i.e., the project minimizing its winning bid, is an important factor to efficiently sustain the parachain. While 27% of teams mentioned in the survey that they will switch to some private form of bidding after they obtained their first slot, improved capabilities in the ecosystem might lead to new forms of auction participation mechanisms. To take the example of parachain-native crowdloan pallets, teams are free to abstract the bidding mechanism from the bonding mechanism and delegate it to specific entities (individuals, smart-contracts or the Council) that aim for optimal bidding. This means that with a growing number of available slots and active parachains, the candle auction mechanism comes to fruition in the near future and increases in its importance.

Appendix:

Events of auctions expressed in block heights

Full table of crowdloans

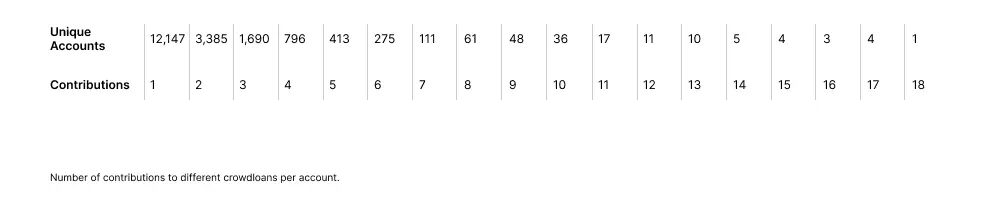

Full table of number of unique contributions per account

Notes

[1]: More precisely: To reduce storage requirements, only every 20th block can be sampled and be selected as the termination block.

[2]: To decrease the storage requirements, those bids are actually only cast on-chain once the candle phase starts.

[3]: There were a few non-serious bids from individually-controlled accounts, which are discarded from the analysis because of their irrelevance.

[4]: Assuming that the percentage of samples corresponds to the percentage of leading blocks.

[5]: To understand this, consider the following example: Team A wants to only bid for lease period 1-4. To stand a good chance against other teams that bid for periods 1-8, it would probably require another Team B that bids for lease period 5-8. However, bidding for period 5-8 (in fact any period not starting at 1) is irrational, because tokens are required to be still locked from period 1. Therefore, for the same amount of bonded tokens, the winning bid could be increased. It would then be more reasonable to directly bid for period 1-8. Sharing slot duration only becomes viable once one team already occupies a slot. Then, the tokens locked in that slot could be used to be both locked in the current slot and for the lease periods at the beginning of the new slot.